In recent years, due to the rapid growth of data volume, many new applications have benefited from the powerful capabilities of HPC (High Performance Computing) to utilize shared resources to perform computationally intensive operations. Compared with traditional computing, HPC can obtain results at lower cost and in a shorter time, and HPC hardware and software have become easier to obtain and more widely used. Therefore, the global HPC market is showing a growth trend.

This trend can be seen from the performance reports of TSMC, a leading global wafer foundry.

01

HPC Becomes a New Favorite of OEM

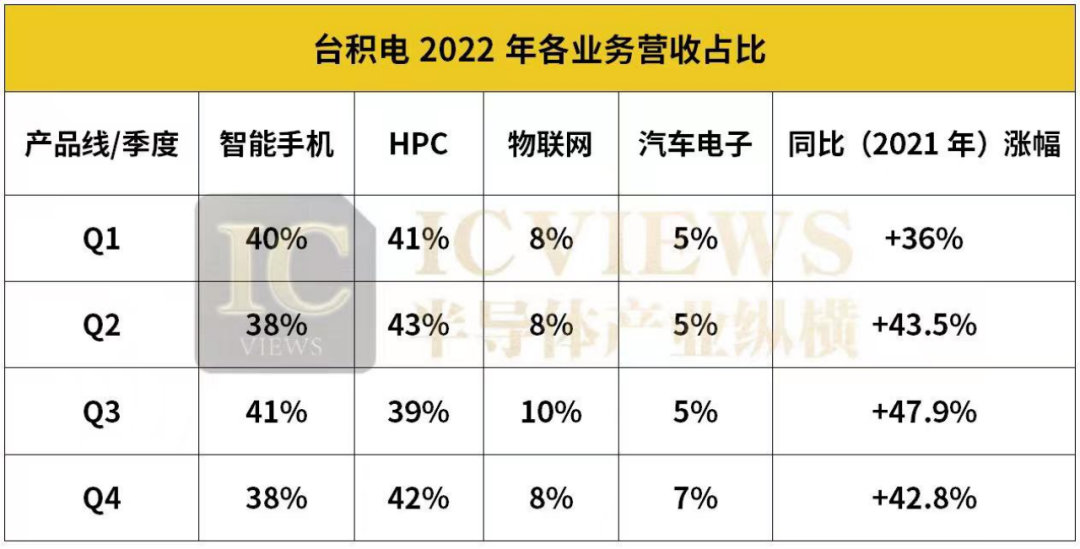

Recently, TSMC announced its revenue for the fourth quarter of 2022. According to product types, TSMC accounted for 38% of smartphone revenue in the fourth quarter, 42% in high-performance computing, 8% in the Internet of Things, 7% in automotive electronics, and 2% in consumer electronics. Among them, high-performance computing performance increased by 10% quarterly, accounting for nearly half of Q4’s revenue share. Among them, the HPC field defined by TSMC includes CPUs, GPUs, and AI accelerators.

It can be seen that in the first quarter of 2022, HPC surpassed smartphones, which had been TSMC’s top revenue source for many years, and has been making significant revenue contributions since then. The strong revenue of this business is attributed to TSMC’s advanced packaging capabilities.

TSMC’s CoWoS technology is a 2.5D wafer level multi-chip packaging technology specifically designed for HPC equipment applications, which has been in production for nearly 10 years. Its traditional CoWoS technology with silicon interlayer (CoWoS-S) has entered the fifth generation. The silicon intermediate layer of CoWoS-S can reach more than twice the full mask size (1700mm2), integrating leading SoC chips with more than four HBM2/HBM2E stacks. It is reported that TSMC has determined that its latest CoWoS process variant, CoWoS-L, is the only solution for 2.5D packaging with 4x full mask size. It is collaborating with HPC chip customers to jointly address the challenges of the substrate end and is expected to begin commercial production from 2023 to 2024.

With CoWoS, TSMC has won a large number of orders from high-performance computing processor suppliers such as AMD and NVIDIA.

In the past two years, AMD has significantly increased its market share in CPUs and GPUs for servers, laptops, and desktops, and has also seen a significant increase in game chip shipments. In order to further grow, AMD not only increased its orders with backend partners and ABF carrier suppliers, but also significantly increased TSMC’s 7nm and 6nm manufacturing orders, and used the 5nm process to manufacture its new product, the Zen4 architecture of the Ruilong 7000, further increasing its revenue contribution to pure wafer foundries. In order to ensure inventory in the event of insufficient production capacity, AMD even booked two years of 5nm and 3nm production capacity in 2021.

On the other hand, NVIDIA has adopted TSMC’s 5nm process for its next generation Adaoverlay architecture RTX40 series GPUs. With the return of NVIDIA orders, in order to successfully complete NVIDIA’s new HPC GPU orders, TSMC’s order volume for advanced packaging materials and heat dissipation materials required for CoWos surged by about three times in 2022, which is also one of the reasons for TSMC’s HPC business doubling growth.

TSMC has previously proposed that high-performance computing (HPC) has a sustained momentum and is expected to become the strongest driving force for long-term growth, bringing the greatest contribution to the company’s revenue growth. The head of HPC business development at TSMC also stated that TSMC expects HPC to continue to be the strongest growth platform until at least 2025 in the future.

02

Chip giants strive to become HPC leaders

HPC was born in an internal data center with the ability to process data at high speeds and perform complex calculations to solve performance intensive problems. In order to become leaders in the HPC field, NVIDIA, AMD, and Intel have also made continuous progress in the HPC application field, with each company’s data center accounting for a significant market share and even setting ambitious goals.

Nvidia: HPC chip performance will increase by 200-250% annually in 2022.

Nvidia has seen significant growth in various fields such as gaming, data centers, artificial intelligence, and autonomous driving in recent years, and its demand for GPU computing power has reached an unprecedented level. With the increasing demand from customers for ultra large scale computing, cloud computing, and AI services, data center services are even gradually surpassing gaming services.

On March 23, 2022, NVIDIA launched its first ARM Neoverse based data center exclusive CPU for HPC and AI infrastructure – the Grace CPU superchip. In the same month, Nvidia acquired Bright Computing Inc. The specific acquisition amount is currently unclear. Throughout Bright Computing, we sell large-scale cluster management software for HPC devices, with platforms that support x86 and ARM based chips, as well as Nvidia’s GPUs, and can be flexibly deployed in data centers, across public clouds, or network edges. Nvidia also stated that this acquisition will produce software for managing HPC systems. Nvidia CEO Huang Renxun stated that the world is going through an “industrial HPC era”.

So far, NVIDIA has launched architectures such as Volta, Ampere, Hopper for HPC and AI training, and has launched high-end GPUs such as V100, A100, and H100 based on this. The Hopper H100 adopts TSMC’s 4 nm process and has 80 billion transistors, far surpassing the Ampere A100 in performance and efficiency. It is a product designed by NVIDIA specifically for supercomputers.

According to NVIDIA’s internal forecast, the performance of HPC chips in data centers will have a high target of annual growth of around 200% to 250% in 2022, including data centers from Hopper architecture and shipments contributed by AI chip solutions.

AMD: By 2025, the energy efficiency of AMD EPYC and AMD Instinct will increase by 30 times.

In February 2022, AMD officially completed its acquisition of Selence. As a manufacturer specializing in CPU and GPU for a long time, AMD will integrate CPU, GPU, FPGA, adaptive SOC, and deep professional software knowledge to provide a leading computing platform for cloud computing, edge, and intelligent terminal devices after acquiring Selence, which has strong capabilities in FPGA, programmable SoC, and ACAP. This marks AMD’s establishment as the leader in high-performance computing in the industry.

AMD has always been committed to leveraging the latest technologies and products in high-performance computing, and currently AMD EPYC has a market share of over 25% in the x86 server CPU market; The Instact ecosystem released last year, as well as the previous ROCm ecosystem, is providing Exascale level (billions of sub tiers) technology to HPC and AI customers with a broad foundation, meeting the growing demand for computing accelerated data center workloads. In addition, AMD is expected to launch 3nm Zen 5 architecture processors from 2023 to 2024.

AMD has also announced an ambitious plan to increase the energy efficiency of AMD EPYC series processors and AMD Instact computing cards by 30 times in artificial intelligence training and high-performance computing applications running on accelerated computing nodes by 2025.

Intel: GPU has become a breakthrough point for its own business growth.

Although the GPU market is dominated by AMD and NVIDIA, Intel also has a lot of technological accumulation in GPU.

Intel’s data center GPU Ponte Vecchio based on Xe HPC microarchitecture is its graphics card product for the high-performance computing market. It is Intel’s most complex SoC to date, consisting of 100 billion transistors, providing leading floating-point operations and computational density to accelerate AI, HPC, and advanced analysis workloads. After NVIDIA launched the Grace CPU, Intel plans to launch an XPU – Falcon Shores architecture chip. The new architecture includes CPU and GPU, which has improved performance by more than five times in memory capacity, computing density, and other aspects. The product is expected to be released in 2024.

Intel has also launched hardware products with different architectures through its XPU strategy, ranging from general-purpose CPUs to dedicated GPUs, ASICs, and FPGAs, supporting the computing power requirements of AI and HPC. In addition, the development trend of the future computing architecture is the integration of CPU and GPU, so as to form the integration mode of interconnection, complementarity and interworking to reduce the communication cost of computing and storage units. As Intel, which has been leading the CPU industry for many years, it also has a unique advantage in this trend. The vision of Intel GPU is gradually becoming clear: in the trend of computing diversification and explosive growth in computing power demand, Intel GPU will become the cornerstone of computing power driving the development of emerging industries, and also become a breakthrough point for Intel’s own business growth.

03

The market potential of HPC chips is enormous

With the use of HPC in the cloud, there will be more applications of HPC in consumer oriented software program development. The emergence of virtual worlds and metaverse concepts has also ushered in new development opportunities for HPC, which can be used for entertainment applications such as gaming (AR/VR) and analog applications such as digital twins. HPC has surpassed smartphones as the main engine of growth in the semiconductor industry, possessing the ability to process data at high speeds and perform complex calculations to solve performance intensive problems.

Various computing devices are becoming ubiquitous, and the amount of data generated and communicated through global networks is increasing exponentially. In order to keep up with this growth, HPC has become crucial and is showing explosive growth. According to Report Ocean, it is expected that the global HPC chipset market size will reach $13.68 billion by 2027, up from $4.3 billion in 2019.

The competition in the HPC chip market is bound to become more intense in the future.