After the Spring Festival, global chip giant Intel released a financial report that was far below market expectations, including the fourth quarter of 2022 and the annual report for 2022.

According to the financial report, in the fourth quarter of 2022, Intel’s total revenue was $14.042 billion, a year-on-year decrease of 31.6%, and its net profit was – $661 million, a year-on-year decrease of 114.3%. And throughout 2022, Intel’s performance was equally dismal, with a full year revenue of $63.1 billion, a 20% decrease from $79 billion in 2021, and a net profit of $8.014 billion, a 60% drop from $19.87 billion in 2021. This financial report is referred to by Wall Street analysts as a “disaster level” financial report.

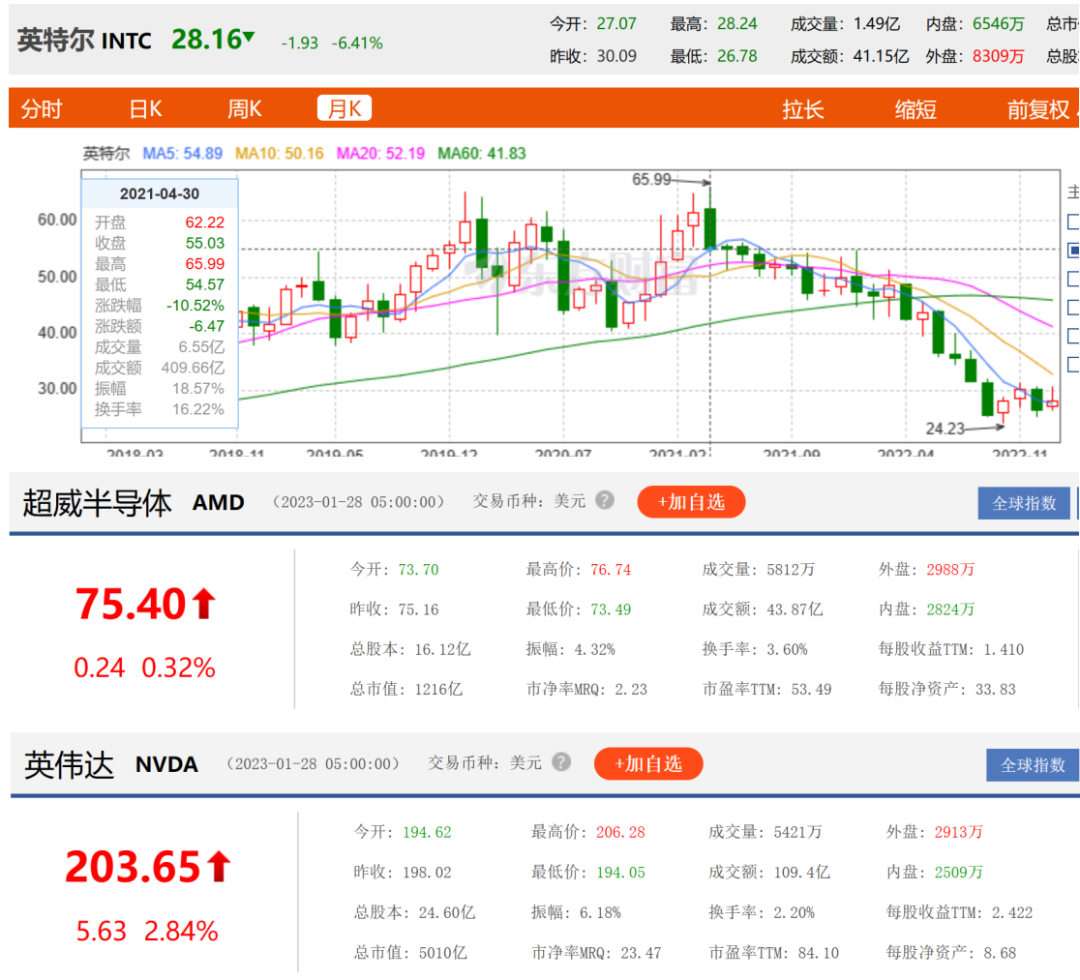

After the financial report was released, Intel plummeted 10.9% during the session on January 27th, narrowing its closing decline to 6.4%. Its competitors AMD and Nvidia rose 0.32% and 2.84% respectively. As of the close on January 28th, Intel’s stock price fell to $28.16 per share, another 6.41% decline. Compared to the high of $65.99 per share in April 2021, it has dropped by 57.3%, and the market value has evaporated by nearly $120 billion.

In fact, the sudden drop in Intel’s stock price is not an unexpected event. Since June 2022, Intel’s stock price has set a record for four consecutive months of continuous decline. The stock prices of Intel’s three equipment suppliers, KLA, Applied Materials, and Fanlin Group, have also fallen by between 2% and 7%. What’s wrong with this chip giant?

Both the market and stock market are killed

The performance in 2022 is Intel’s worst annual report in more than 20 years, without one.

Judging from Intel’s performance in the fourth quarter of 2022, the worst may come later. Because even after adjustment, the net profit for this quarter was only $400 million, a significant decrease of 92% compared to $4.7 billion in the same period in 2021!

According to the fourth quarter financial report of 2022, Intel’s quarterly revenue of $14.042 billion decreased by 32% compared to $20.53 billion in the same period of 2021; The net loss was $661 million, while the net profit for the same period in 2021 was $4.623 billion. From a specific performance perspective, as Intel’s largest “cash cow” division, Intel’s customer computing business group, had a net revenue of only $6.625 billion in the fourth quarter, compared to $10.333 billion in the same period of 2021, a decrease of 36% year-on-year. The annual revenue was $31.7 billion, a decrease of 23% year-on-year.

Another major “cash cow” division, Intel Data Center and Artificial Intelligence (AI) business group, also experienced a 33% decline in revenue in the fourth quarter, from $6.426 billion in the same period in 2021 to $4.304 billion. The decline in revenue for two key departments has raised concerns among investors and analysts.

The transcript for the fourth quarter of 2022 falls far short of market expectations. However, Intel CEO Pat Kissinger stated that this is not the worst, and the performance in the first quarter of 2023 will be lower than expected, mainly due to the difficult environment leading to excess chip inventory.

Kissinger provided guidance for the first quarter of 2023, with revenue ranging from $10.5 billion to $11.5 billion, far below the previous market expectation of $14 billion and far below the $18.35 billion revenue in the first quarter of 2021. It is expected that the gross profit margin will be only 34.1%, much lower than the 55.2% it was a year ago. From Intel’s guidance, it can be seen that Intel expects to continue to lose money in the first quarter of 2023. This is also the first time in nearly 30 years that Intel has suffered losses for two consecutive quarters.

After the release of Intel’s performance guidelines, some Wall Street analysts called the guidelines a “historic collapse” of Intel, which could trigger a sell-off in chip stocks and potentially lead to a collapse in Intel’s stock price. No language can describe or explain Intel’s historic collapse, “said a Wall Street analyst on Intel’s newly released financial report. Because on a quarterly basis, Intel’s performance is showing an accelerating downward trend. In the fourth quarter of 2022, Intel’s revenue decreased by more than 30%, while in the third quarter, the revenue decreased by 15%. In terms of net profit, the third quarter decreased by 59%, while in the fourth quarter, the decline was 92%.

The concerns of Wall Street analysts are not unreasonable. In 2022, Intel’s total revenue was surpassed by TSMC for the first time, and its net profit also lagged behind TSMC at NT $295.9 billion (approximately $9.8 billion). And TSMC is mainly engaged in wafer foundry, with a market value more than four times that of Intel. The continuous decline in market value has also led to Intel’s total market value falling behind its old rival AMD, and also far behind NVIDIA. Intel will face a “double kill” in the market and stock market in 2022.

Is it okay to leave the Chinese market?

The “sustained macro headwind” is the main reason for Kissinger’s poor performance outlook, regardless of the reason, Intel’s chip inventory surplus has become the main reason for its poor performance.

According to Bernstein data, Intel’s current inventory value is $13.2 billion, equivalent to approximately 151 days of inventory. This inventory quantity and inventory time are rare in the industry. Some financial institutions have also pointed out that Intel, even though it is aware of the high level of inventory in its channels, continues to overship even though there are clear signs of market collapse using prices and production capacity as weapons. This’ semi destructive ‘behavior can bring heavy pressure to one’s own operations.

After providing performance guidance for the first quarter of 2023, it sparked market panic, causing capital markets to move and stock prices to continue to decline. However, Kissinger is optimistic about the rebound in performance in the second half of 2023, mainly due to the recovery of the Chinese economy and increased demand from government customers and large enterprises. But Intel refused to provide full year performance guidance due to the turbulent global economic situation.

Since 2015, the Chinese market has become Intel’s largest market. Since 2011, China has become the world’s largest PC market with a massive data center business. But what Kissinger didn’t mention was that Intel’s performance in the Chinese market was also poor. In 2022, the revenue of the Chinese Mainland market fell by 25% compared with 2021.

With China’s “liberalization”, the Chinese economy will experience a recovery, and the recovery of the Chinese economy, which has become Intel’s largest market for 7 consecutive years, is a great benefit for Intel. But Shi Baogang, the founder of Botong Lianchuang (Beijing) Technology, who has been engaged in PC trading for many years, does not believe that Intel’s performance in the Chinese market will fundamentally change. In recent years, trade frictions between China and the United States have targeted ethnic brands such as Huawei, which has led to a genuine resistance from Chinese consumers towards American brands. This is also the main reason why Intel’s performance in the Chinese market has also declined. Even if China’s economy recovers, it is difficult to bring substantial changes to Intel’s performance Shi Baogang believes that the treatment suffered by national brands such as Huawei in the United States has given many Chinese consumers a spontaneous sense of exclusion from American brands. Intel’s development in the Chinese market is still full of variables, and all hope is placed on the recovery of the Chinese market or Intel’s willingness.

Intel’s large inventory and underperforming performance have led to a change in its rating by many institutions. Barclays analyst Blayne Curtis has lowered Intel’s target price from $30 to $27 and maintained a “hold and see” rating for the stock. And its old rival AMD was rated as a ‘buy’. JPMorgan Chase has lowered Intel’s target price from $32 to $28, reiterating its underweight rating. Rosenblatt lowered Intel’s target price from $20 to $17 and maintained its sell rating. For a while, Intel suffered from the decline of many institutions.

But there are also analysts who support Intel. UBS analyst Timothy Acuri said that Intel’s first quarter was so bad, and we believe this is already the bottom, and there may be a bottom rebound soon.

PC entering the cold winter?

As a global CPU giant, Intel’s performance is closely related to the downstream PC and server markets, which are also the two most important markets for Intel. However, after experiencing a period of rapid growth globally, both markets have started to show sluggish performance.

Counterpoint Research is an international and authoritative market research organization that released relevant data on the PC end in early 2023. The data shows that global PC shipments in 2022 were 286 million units, a significant decline of 15% compared to 341 million units in 2021. Especially in the fourth quarter of 2022, global PC shipments reached a new low in nearly a decade, with a year-on-year drop of 28%. It is worth mentioning that this is the fourth consecutive quarterly decline in global PC shipments.

Based on the performance of the top three global PC operators Lenovo, HP, and Dell in the fourth quarter of 2022, it is not difficult to understand the sharp decline in global PC shipments. In the fourth quarter of 2022, Lenovo and HP’s shipments both decreased by 29%, while Dell’s shipment decline was even more astonishing, reaching 37%. Among the top five manufacturers, only Apple’s shipment volume decreased by a single digit of 3%, with the lowest drop of 23% for other manufacturers and nearly 30% for other brands.

Throughout 2022, the revenue of Intel’s PC related client computing division reached $31.7 billion, a year-on-year decrease of 23%, but in the fourth quarter, the decline was as high as 36%; The global PC business is declining, and the impact on Intel is evident to the naked eye.

Due to the global economic downturn, companies are experiencing a significant reduction in their spending on data centers, and the procurement of office computers is also slowing down. This can be seen from the decline in global PC shipments for multiple consecutive quarters. Some institutions predict that PC shipments will continue to decline in 2023, and it is not expected to resume growth until 2024.

Intel, which was originally the “big brother” in the server chip market, has also encountered cannibalization from competitors such as AMD. In the first half of 2022, Intel’s total revenue was $15.321 billion, a decrease of 21.96%. The net loss was $454 million, a year-on-year decrease of 108.97%. However, AMD, its old rival, saw a revenue growth of 70.13% over the same period, showing sustained growth in its market share in mobile laptops, desktops, servers, and the entire x86 market.

Especially in terms of x86 processor market share, AMD has increased to 31.4%. The month on month increase of 3.7% and the year-on-year increase of 8.9% indicate that Intel’s market share in this field has fallen below 70% for the first time, indicating that the competition between the two companies is becoming increasingly fierce.

According to data from third-party institutions, AMD has achieved growth in the server market almost every quarter in the past two years due to multiple delays in the release of Intel’s fourth generation Xeon processors, and its overall share has now reached double digits. As Intel’s market share continues to decline and its competitors continue to rise, this is also the reason why analysts expressed shock.

High level fluctuations, layoffs, and cost reductions

The expected poor performance of Intel in 2022 and the first quarter of 2023 may be the main reason for Chairman Omar Ishrak’s resignation. Prior to his resignation, he appointed Frank Yery as a board member to replace him. The turmoil in Intel’s senior management has also raised concerns among investors.

Because the current CEO of Intel, Kissinger, was supported by Omar Ishrak to take that position. Kissinger has repeatedly publicly stated that Omar Ishrak played an important role in appointing him as CEO. It is not yet known whether the departure of Omar Ishrak, Kissinger’s “big backer”, will have an impact on Kissinger’s future work. However, the working atmosphere cultivated by Omar Ishrak in the board and management team, or what Frank Yery is currently struggling to achieve, is still unknown.

Despite poor performance and fluctuating executives in 2022, Intel still paid a dividend of $6 billion. It should be noted that Intel’s net profit for the entire year of 2022 was only $8.014 billion, indicating a decline in profitability. Paying such a large dividend directly led to a decline in Intel’s cash flow. The financial report shows that the net cash flow generated from operations during the reporting period was $15.43 billion, compared to $29.46 billion in 2021, a year-on-year decrease of $14.03 billion. Under pressure on the fourth quarter’s performance, organic organizations question whether it is reasonable for Intel to pay a high dividend at this time, and some analysts even believe that Intel should cut its dividend.

But Kissinger does not agree with the views of institutional analysts and cannot accept Intel’s suggestion of sacrificing dividend payments to turn losses into profits.

Kissinger emphasized that Intel is committed to distributing dividends and providing healthy and competitive dividends. Intel’s long-term strategic investment is the foundation for Intel to return dividends to shareholders, in order to achieve Intel’s overall capital allocation.

In the context of a decrease in net cash flow inflows, a sharp drop in net sales profit from 25.14% in 2021 to 12.71% in 2022, and a surge in sales expenses of 310% year-on-year, Intel inevitably faces significant operational pressure, and reducing costs and increasing efficiency has become a challenge that Intel has to face. There are reports that Intel plans to reduce costs by $3 billion this year, with a total annual capital expenditure of approximately $20 billion. In order to reduce expenses, Intel has also joined the wave of layoffs in Silicon Valley. Hundreds of jobs located in Silicon Valley will be laid off, and layoffs began at the end of last year, followed by another layoff. Whether there will be further layoffs in the future is uncertain.

Due to the impact of cost expenditures, Kissinger’s plan to build Intel chip factories may also be affected. The construction plan for the German factory has been postponed, and according to German media reports, Intel is now seeing a “difficult market situation” and cannot promise to continue advancing the plan to build a semiconductor factory in Germany in the first half of this year.

Reducing costs is a double-edged sword, and while reducing costs, some opportunities will be lost. However, based on Intel’s current situation, it seems that there is no better way. As for the performance of the Chinese market, which Kissinger has high hopes for, in the second half of this year, we will wait and see.https://www.stoneitech.com/