Recently, the prices of silicon wafers, which have been consistently strong, have continued to decline.

Silicon wafers are essential raw materials for the production of wafer fabs such as TSMC, Intel, Samsung, and Liandian. They are a key indicator for observing the dynamics of semiconductor prosperity, especially the spot price, which is closer to the current market situation and better reflects market dynamics in the first place than the contract price.

The downward trend in the prices of silicon materials and silicon wafers, which began in November last year, seems unstoppable. Is this rapid and rapid decline still beyond market expectations, and will the trend continue? What kind of impact has it brought?

01

How did it fall

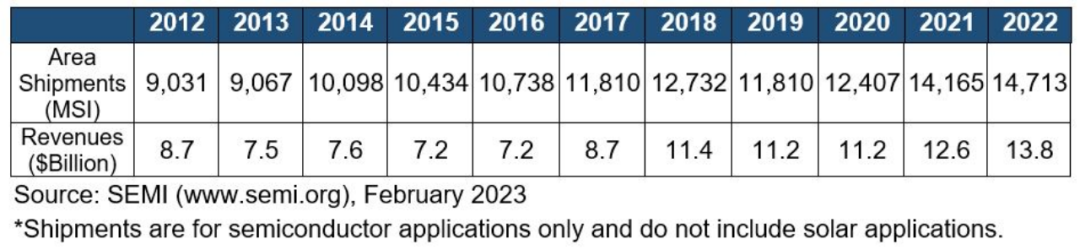

SEMI recently reported that global silicon wafer shipments and revenue set new records in 2022. In 2022, global silicon wafer shipments increased by 3.9% to 14.713 billion square inches (MSI), while wafer revenue increased by 9.5% to $13.8 billion during the same period. Last year, the total number of MSIs was 14713, while the shipment volume in 2021 was 14165 MSIs, as silicon wafers supported strong demand for semiconductor equipment. The consumption of 8-inch and 12-inch wafers has increased, partly due to the automotive, industrial, and IoT sectors, as well as 5G construction. Wafer revenue reached $13.831 billion, surpassing the previous record set in 2021.

Anna Riikka Vuorikari Antikainen, Chairman and CEO of SEMI SMG, said, “Despite increasing global macroeconomic concerns, the silicon wafer industry continues to grow. Over the past decade, silicon shipments have grown for nine years, demonstrating the core role of silicon wafers in the crucial semiconductor industry

But the prices of silicon wafers, which have been consistently high, have shown signs of falling recently. According to media reports, the spot prices of silicon wafers have recently started to decline for the first time in more than three years, mainly involving 6 inches, 8 inches, and 12 inches.

South Korean chip manufacturers Samsung and SK Hynix are planning to purchase fewer silicon wafers for chip production than originally planned. It is said that this plan was discussed as early as last quarter.

Currently, there are five major suppliers of wafers; Shin Etsu and Sumco from Japan, GlobalWafers from Taiwan, China, China, Siltronic from Germany and SK Siltron from South Korea.

During the two most severe years of the epidemic, the supply of these wafers was tight, and chip manufacturers were in short supply.

This situation continued when the global economy began to decline in 2022. This is because silicon wafers are a back-end industry, and the impact of the consumer market comes later than that of the front-end industry.

In the third quarter of last year, when chip manufacturers first reported a decline in profits, wafer companies saw an increase in profits.

Chip manufacturers are seeking to reduce the number of wafers they purchase more than usual. Sources say that wafer supply transactions are usually long-term, which typically limits chip manufacturers from adjusting their purchase quantities, but Samsung and SK Hynix have requested further reductions.

Silicon wafer manufacturer Sumco stated that demand from automotive and industrial customers remains strong, but the weak smartphone market may generate lower wafer orders in 2023 and then recover in 2024. The recent continuous inventory adjustments have dealt a heavy blow to the storage chip manufacturing industry and may continue for several months, “said Sumco CEO Masayuki Hashimoto

What is the reason for the decline in silicon wafer prices?

The most direct reason is the excessive inventory of downstream customers. Silicon chip manufacturers have stated that as early as the fourth quarter of 2022, customers’ capacity utilization rates had significantly decreased. The current inventory held by customers is too high and needs to be restocked. Some foundry companies hold inventory of silicon wafers for up to five to six months, which is too much. Of course, they won’t want to buy more products, or even negotiate.

In the first quarter of 2022, silicon wafers remained in short supply in the semiconductor industry chain. At that time, Global Crystal, the world’s third largest semiconductor wafer manufacturer, even stated that its long-term production capacity from 2022 to 2024 had been sold out. The International Semiconductor Industry Association SEMI predicts that global silicon wafer shipments will reach a historic high of nearly 147 million square inches in 2022.

However, in the fourth quarter of 2022, the decline in spot prices of silicon wafers was the result of a chain reaction, as demand for end products continued to weaken.

It is understood that the current demand for the weakest 6-inch silicon wafers has seen the largest drop in spot prices this quarter, with a single digit decline. The average price of 8-inch silicon wafers has not changed much. The spot price of 12 inch silicon wafers is relatively stable, but industry insiders have stated that customers have requested a price reduction and intensive negotiations are underway.

Chen Jiahui, a silicon industry analyst at the Silicon Industry Branch of the China Nonferrous Metals Industry Association, said that the fundamental reason for the significant decline in silicon wafer prices is the price reduction of silicon materials. According to data from the Silicon Industry Branch, silicon wafer prices showed a circuit breaker decline in the third week of December. In addition, silicon chip leaders TCL Central and Longji Green Energy have also continued to lower silicon chip prices.

Due to the influx of a large number of new players and new production capacity in the silicon wafer industry, there was concern about price wars at the end of last year. However, due to the continuous rise in silicon material prices, objective conditions did not support the price reduction of silicon wafers for most of this year; With the recent increase in silicon material supply and the growth of silicon wafer inventory, it is inevitable that silicon wafer prices will decrease.

02

Falling price impact

On February 8th, data from the Silicon Industry Branch of the China Nonferrous Metals Industry Association showed that the price of silicon materials continued to rise this week, with an increase of about 11%. Since January 18th, silicon material prices have been rising for four consecutive weeks. However, throughout the year, the overall supply of silicon materials is still in a state of oversupply, and the downward trend at the annual level has not changed.

The first benefit from the price reduction of monocrystalline silicon wafers is, of course, downstream photovoltaic cells. The cost of silicon wafers accounts for approximately 50% of the cost of photovoltaic cells, while battery cells account for approximately 65% of component costs. Lowering prices will create a driving force that is transmitted layer by layer from top to bottom, forming a “domino effect”, ultimately benefiting applications such as photovoltaic cells and power stations. If the price reduction of silicon wafers this time is a linkage effect caused by the reduction of silicon materials, then the gross profit of downstream components is expected to increase and the profitability is expected to be repaired.

In the second quarter of 2022, the gross profit margin of Longji Green Energy’s silicon wafer business was approximately 21%, compared to 24% in the first quarter. The decrease was due to the further increase in silicon material prices in the second quarter; The gross profit margin of the component business is 12%, a decrease of about 6 percentage points compared to the first quarter, due to the impact of price increases in upstream silicon materials and silicon wafers.

TCL Central faces the same problem, with its gross profit margin for silicon wafers and components in the first half of 2022 being 18.37% and 7.69%, respectively, a year-on-year decrease of 3.09 percentage points and 4.83 percentage points, also affected by the continuous rise in upstream silicon material prices.

From the perspective of technology and funding barriers in all aspects of the entire industry chain, the highest barriers are in order of polycrystalline silicon, batteries, long crystals, and components. In an equilibrium state, the ranking of reasonable profit margins is roughly distributed in this order. The previous stage was a difficult period for battery and component companies. With the price reduction in the upstream market, the most difficult stage has passed, and the profits of battery and component companies will enter an upward channel.

According to the research report of China CITIC Construction Corporation, the supply of silicon materials is expected to become increasingly surplus. It is expected that the total production of silicon materials in 2023 will be about 1.45 million tons, corresponding to over 550GW of producible components. By the end of the year, the total production capacity of silicon materials will reach 2.48 million tons, corresponding to around 1000GW of producible components, significantly exceeding demand. The annual downward trend of silicon material prices has not changed. At present, the price of silicon materials may stabilize in the first quarter, but as the supply of silicon materials becomes increasingly abundant, it still shows a downward trend.

The Silicon Industry Branch said that the periodic market price of silicon materials will still fluctuate according to the actual installation rhythm of the terminal, the production progress of each link of the industrial chain, the adjustment of the operating rate, the degree of inventory digestion and other factors. It is expected that the situation of oversupply in each link of the industrial chain in the second and third quarters of this year will be more prominent.

Industry insiders say that the price reduction of silicon wafers will reshape the value logic of the entire industry chain. The new silicon material production capacity continues to be released, and the level of upstream competition is becoming increasingly fierce. The silicon wafer process is still in the process of rapid price decline. Assuming that the decline in silicon wafer corresponds to the decline in silicon material prices, it is feared that the current level of silicon material prices may be difficult to cover temporarily. However, in the current complex market environment and rapid changes, upstream enterprises are also seeking and exploring new business cooperation models, seeking mutual support and binding cooperation relationships.

In addition, a price war is imminent, and the impact on the component side will be significant. The continuous decline in prices of silicon materials and silicon wafers will drive industry profits back to a reasonable distribution level. On December 21st, a third-party institution PV InfoLink analyzed and pointed out that in the context of steadily increasing silicon material supply scale, the upstream sector is facing market changes with rapidly shrinking demand for silicon wafer materials. Since December, the level of upstream competition has become increasingly fierce, and the prices of silicon wafers have rapidly declined. After forming a price stampede, a price war mode has been initiated. Assuming that the decline in silicon wafers corresponds to the decline in silicon material prices, the current level of silicon material prices may be difficult to cover.

PV InfoLink believes that even in the market environment of sharp and rapid decline in silicon wafer prices, the current silicon wafer industry still faces the dilemma of its own abnormal inventory levels being high and crops being forced to decline due to insufficient demand.

Wafer foundry may also face a price war. Samsung’s chip business saw a sharp drop in profits of over 90% in the previous quarter, but its wafer manufacturing business, which competes with TSMC, achieved record high revenue in the previous quarter and the entire year last year. Last year’s profits also increased, reflecting the expansion of advanced process capacity and a more diversified customer and application field.

However, Samsung admitted that it is difficult to escape the pressure of industry inventory adjustment this quarter, which will cause the capacity utilization rate of wafer foundry business to begin to decline. The industry is concerned that Samsung may launch a price reduction and order grabbing strategy, which will be detrimental to Taiwan’s TSMC, Liandian, and other manufacturers.

Industry analysis shows that the capacity utilization rate of wafer foundries has generally declined recently, and the capacity utilization rate of Liandian has shifted from the previous full load situation to a downward trend of around 70%. It has been reported that some manufacturers have only 50% of their production line capacity utilization rate left, but TSMC and Liandian have both adhered to their prices. TSMC has increased prices by 6% this year, and Liandian expects the average product price (ASP) to remain unchanged this quarter.

In the current situation of poor terminal demand and hard wafer prices, if Samsung cuts prices to grab orders, it is very attractive for IC design companies and integrated component (IDM) factories that are facing huge inventory pressure and unwilling to pay more manufacturing costs. Samsung can not only fill the capacity gap, but also help increase market share.

Samsung did not provide relevant data and pricing updates on its wafer foundry capacity utilization rate. It only revealed the adjustment of industrial inventory, which has led to a decline in wafer foundry business capacity utilization rate. However, it still expects a recovery in demand from automotive and high-speed computing in the second half of the year, and will win new customers with the competitiveness of the second-generation 3nm process products. It has established an advanced packaging team to support the wafer foundry business needs.